MENU

MENU

2.2 Operational Framework of Monetary Policy

The funding need of the system, which was TRY 93.1 billion as of end-2018, decreased by TRY 9.5 billion throughout 2019 to TRY 83.6 billion by end-2019. In the framework of OMO, the CBRT provided funds via one-week repo auctions and the Primary Dealer Liquidity facility. In this period, the overnight repo rate at the BIST Repo-Reverse Repo Market was around the policy rate, the one-week repo auction rate. Taking into account the developments in financial markets, the one-week repo auctions were halted twice with announcements on 22 March 2019 and 9 May 2019.

Banks continued to use the facility which allows repo transactions to be changed into deposit transactions. The swap facilities with the CBRT acting as a counterparty have provided flexibility for banks in FX risk and liquidity management, supported the effectiveness of the monetary transmission mechanism contributing to decreasing demand-supply imbalances on the swap market and keeping market rates aligned with the policy rate.

To increase flexibility in the banking sector’s collateral management, in January 2019, the discount rates for government domestic debt securities (GDDS) and lease certificates issued in Turkey by the Asset Leasing Company of the Turkish Treasury (ALCTT) accepted as collateral against TL transactions, which used to be 5% for all maturities, were re-arranged depending on their maturities. Accordingly, the discount rates for securities with a maturity less than two years, securities with a maturity between two and five years, and securities with a maturity longer than five years were set at 1%, 2%, and 3%, respectively.

An overall Turkish lira portfolio target of nominal TRY 18.9 billion was set for end-2019. The OMO portfolio, which was at nominal TRY 15.40 billion level at the beginning of 2019, purchased TRY 6.60 billion worth of nominal instruments, bringing the year-end OMO portfolio to TRY 19.37 billion.

As of 27 May 2019, the CBRT started to conduct overnight reverse repo transactions in addition to overnight repo transactions at the BIST Committed Transactions Market in which TL-denominated lease certificates issued by the Ministry of Treasury and Finance as well as by asset leasing companies established by the public enterprises are traded.

At the end of a collaborative work work of the Ministry of Treasury and Finance, the CBRT, the Turkish Banks Association (TBB), the Turkish Capital Markets Association (TSPB), Istanbul Settlement and Custody Bank (Takasbank) and Borsa Istanbul, the TLREF-Turkish Lira Overnight Reference Rate started to be calculated and used as of 17 June 2019 in order to meet the need for a Turkish Lira short-term reference rate with high transaction volume that can be used as a benchmark in debt instruments, financial derivatives, and various financial contracts.

The floating exchange rate policy continued in 2019. Therefore, exchange rates are determined by supply and demand conditions in the market. Under the current exchange rate policy, the CBRT has no nominal or real exchange rate target. Nevertheless, in order to curb risks to financial stability, the CBRT does not remain indifferent to excessive appreciation or depreciation of the Turkish lira.

In 2019, the CBRT did not conduct FX buying or selling transactions, neither directly nor via auctions.

In the first three months of the year, FX deposit auctions against TL deposits were held and the total maximum temporary FX liquidity provided for banks was USD 2.5 billion. Nevertheless, as a result of developments in international markets in March, the Turkish lira funding amount requested by banks from the CBRT increased, thus it was decided that there was no longer need for FX deposit auctions against TL deposits and those auctions were suspended. Moreover, in the same period, in order to limit the adverse impact of the supply-demand imbalances in foreign swap markets on swap rates, the total TL swap sale limit in the CBRT’s TL swap market was increased gradually to 40% from 10% for swap transactions that had not matured.

As of May, swap transactions with maturities longer than 1 week in US dollars and Euro started to be conducted at the Borsa Istanbul Swap Market concurrent with the CBRT’s policy rate. As of 31 December 2019, the amount of swap transactions intermediated by the CBRT at the Borsa Istanbul Swap Market was USD 8.8 billion. In August, it was announced that Turkish lira currency swap transactions, which were executed with one-week maturity via quotation method, would also be executed with 1, 3 and 6-month maturities via the traditional auction (multiple-price) method. The total limit of outstanding swap transactions at the Turkish Lira Currency Swap Market was lowered to 20% of banks’ total transaction limits at the Foreign Exchange and Banknotes Markets and a limit of 20% was defined for transactions to be conducted via the auction method. In 2019, six auctions were held with a total outstanding amount of USD 5.75 billion. The interest rates at the auctions have been consistent with market rates.

In 2019, the US dollar buying rate on FX deposits as collateral was gradually lowered from 2.25% to 1.50%. The US dollar deposit-selling rate was gradually lowered from 4.25% to 3.50% for one-week maturity and from 5% to 4.25% for one-month maturity.

The Turkish lira-settled forward foreign exchange sale auctions that the CBRT started to hold at the Derivatives Market (VIOP) operating under Borsa İstanbul (BIST) on 31 August 2018, continued in 2019 in line with the market conditions.

In order to increase the effectiveness of banks’ liquidity management and contribute to bringing out gold savings into the financial system, the Turkish Lira Gold Swap Market (for transactions on the buy side) was opened in May, and the Foreign Exchange Gold Swap Market (for transactions on both the buy and sell sides) was introduced in October. Transactions at both markets are conducted with banks within their limits and via the quotation method with one-week maturity.

On 31 December 2019, the total stock amount at the Turkish Lira Gold Swap Market was 5 tons. The stock amount at the Foreign Exchange Gold Swap Market was 28 tons on the buy side and there were no transactions on the sell side. In 2019, gold buying and selling against FX and gold buying against Turkish liras continued as well.

The remuneration rate for US dollar-denominated required reserves, reserve options and free deposits held at the CBRT was decreased from 2% to 1% on 5 August 2019; and to 0% on 19 September 2019.

The swap agreement, which had been signed between the Central Bank of the Republic of Turkey (CBRT) and Qatar Central Bank (QCB) on 17 August 2018, was amended on 25 November 2019 and the overall limit was increased from USD 3 billion equivalent of Turkish lira and Qatari riyal to USD 5 billion equivalent of Turkish lira and Qatari riyal.

The CBRT continued to use reserve requirements effectively as a macroprudential tool to support financial stability throughout 2019.

In January, deposits/participation funds of official institutions were excluded from the liabilities subject to reserve requirements, and Provisional Article 6 of the Communiqué on Reserve Requirements was revoked considering the significant decline in the liabilities under this article.

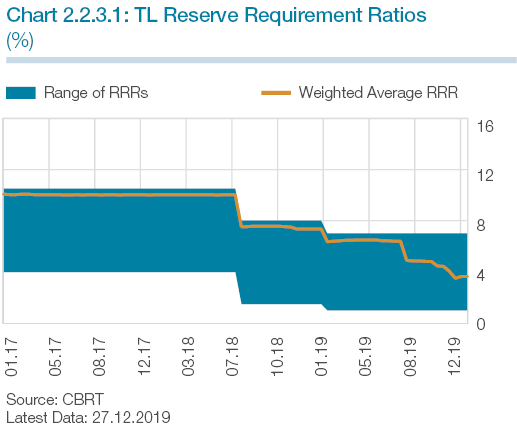

In February, Turkish lira reserve requirement ratios were reduced by 100 basis points for deposits and participation funds with maturities up to 1 year and for other liabilities with maturities up to (and including) 3 years, and by 50 basis points for all other liabilities subject to reserve requirements. Thus, the market was provided with a total liquidity of TRY 3.3 billion and 2.3 billion of FX and gold (Table 2.2.3.1). Moreover, the upper limit of the facility of holding standard gold converted from wrought or scrap gold collected from residents was increased from 5% to 10% of Turkish lira reserve requirements.

In April, the coverage of deposits/participation funds of official institutions excluded from liabilities subject to reserve requirements was expanded to include deposits/participation funds of official institutions subject to the Public Treasurership Regulation.

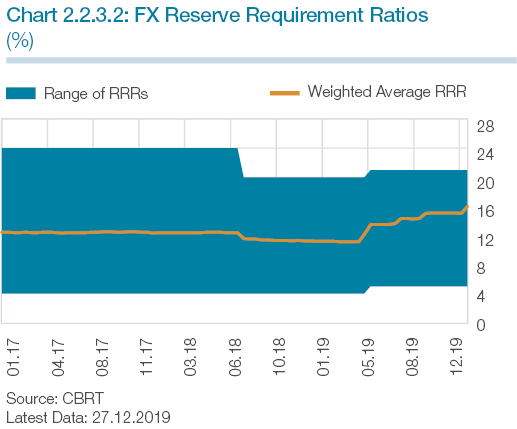

In early May, the upper limit for the FX maintenance facility within the reserve options mechanism was lowered from 40% to 30% and reserve requirement ratios for FX liabilities were increased by 100 basis points for all maturity brackets (Table 2.2.3.2). At the end of May, reserve requirement ratios for FX deposits/participation funds were increased by 200 basis points for all maturity brackets (Table 2.2.3.2). With these implementations, liquidity at the amount of TRY 7.2 billion and USD 4.4 billion was withdrawn from markets.

In June, the TL and FX reserve requirement ratios for financing companies were set as 0% in all maturities.

In July, reserve requirement ratios for FX deposits/participation funds were increased by 100 basis points for all maturity brackets and as a result, a total of USD 1.4 billion was withdrawn from the market (Table 2.2.3.2).

In July, with the amendment to Law No.1211 on the Central Bank of the Republic of Turkey, in addition to liabilities, on- or off-balance sheet items of banks and other financial institutions deemed appropriate by the CBRT were made eligible for reserve requirements.

In August, the reserve requirement ratios for Turkish lira liabilities and the remuneration rates for Turkish lira-denominated required reserves were linked to the annual growth rates of the total of banks’ Turkish lira-denominated standardized cash loans and cash loans under close monitoring, excluding foreign currency-indexed loans and loans extended to banks. Accordingly, the reserve requirement ratio for Turkish lira liabilities for banks with a loan growth between 10% and 20% (reference values) was set at 2% in all maturity brackets excluding deposits and participation funds with 1-year or longer maturity and other liabilities with longer than 3-year maturity (Table 2.2.3.1). Additionally, the remuneration rate applied to Turkish lira-denominated required reserves was set at 15% for banks with a loan growth between the reference values and at 5% for others. With this new method, banks’ loan growth rates were calculated in each reserve requirement period and the banks whose loan growth was between the reference values would be subject to the related reserve requirement ratios and remuneration rates in the next three-months (six reserve requirement periods). With this revision, approximately TL 5.4 billion and USD 2.9 billion equivalent of gold and FX liquidity were provided in the market.

Table 2.2.3.1: TL Reserve Requirement Ratios

Date of Effect |

Deposits/ Participation Funds |

Borrower Funds of Investment Banks |

Other Liabilities |

|||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Maturity up to 3 months |

Maturity up to 6 months |

Maturity up to 1 year |

Maturity of 1 year and longer than 1 year |

Maturity up to 1 year (İnc. 1 year) |

Maturity up to 3 years (incl. 3 years) |

Maturity longer than 3 years |

||||||||||

27.07.2018 |

8.0 |

5.0 |

3.0 |

1.5 |

8.0 |

8.0 |

4.5 |

1.5 |

||||||||

08.02.2019 |

7.0 |

4.0 |

2.0 |

1.0 |

7.0 |

7.0 |

3.5 |

1.0 |

||||||||

09.08.2019* |

2.0 |

7.0 |

2.0 |

4.0 |

2.0 |

2.0 |

1.0 |

1.0 |

2.0 |

7.0 |

2.0 |

7.0 |

2.0 |

3.5 |

1.0 |

1.0 |

*TL reserve requirement ratios for banks fulfilling the real credit growth criteria stipulated in Communiqué No.2019/15 and banks fulfilling the criteria stipulated in Communiqué No. 2019/19 that took effect on29.11.2019 , reserve requirement ratios for Turkish lira liabilities were set at 2% across all maturity brackets excluding deposits and participation funds with a one-year or longer maturity and other liabilities with a maturity longer than three years.

In September, reserve requirement ratios for FX deposits/participation funds were increased by 100 basis points for all maturity brackets, by which liquidity at the amount of USD 1.4 billion was withdrawn from the market (Table 2.2.3.2).

In October, the remuneration rate applied to Turkish lira-denominated required reserves was decreased by 500 basis points and determined as 10% for banks with a loan growth rate within the reference values and to 0% for other banks.

In early December, in order to underpin financial stability by encouraging the channeling of loan supply to production-oriented sectors rather than consumption-oriented ones and reduce the need to update the reference rates, a revision was made in the reserve requirement practice based on credit growth. Accordingly, banks will be able to benefit from reserve requirement incentives under the following conditions:

a) For banks with a real annual loan growth rate above 15%: If their adjusted real loan growth rate, which is calculated by deducting the entire real changes in commercial loans with a 2-year and longer maturity and housing loans with a 5-year and longer maturity from the numerator of the growth rate formula, is below 15%,

b) For banks with a real annual loan growth rate below 15%: If their adjusted real loan growth rate, which is calculated by deducting 50% of the real change in retail loans excluding housing loans with a five-year and longer maturity from the numerator of the growth rate formula, is above 5%.

It was also decided that the real annual growth rate of loans would be calculated based on the last three-month average of the real cash loan stock values, and the calculations would exclude the loans extended to financial institutions.

At the end of December, reserve requirement ratios for FX deposits/participation funds were increased by 200 basis points and, in order to make sure that banks fulfilling the loan growth conditions are not affected by this increase, these ratios were applied 200 basis points lower for banks fulfilling the loan growth condition (Table 2.2.3.2). With this revision, USD 2.9 billion of liquidity was withdrawn from the market.

Table 2.2.3.2: FX Reserve Requirement Ratios

Date of Effect |

Deposits/ Participation Funds |

Borrower Funds of Investment Banks |

Deposits/ Participation Funds |

||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

Maturity up to 1 year |

Maturity of 1 year and longer than 1 year |

Maturity up to 1 year (inc. 1 year) |

Maturity up to 2 years (inc. 2 years) |

Maturity up to 3 years (inc. 3 years) |

Maturity up to 5 years (inc. 5 years) |

Maturity longer than 5 years |

|||||

27.07.2018 |

12.0 |

8.0 |

12.0 |

20.0 |

15.0 |

10.0 |

6.0 |

4.0 |

|||

03.05.2019 |

13.0 |

9.0 |

13.0 |

21.0 |

16.0 |

11.0 |

7.0 |

5.0 |

|||

17.05.2019 |

15.0 |

11.0 |

15.0 |

21.0 |

16.0 |

11.0 |

7.0 |

5.0 |

|||

26.07.2019 |

16.0 |

12.0 |

16.0 |

21.0 |

16.0 |

11.0 |

7.0 |

5.0 |

|||

20.09.2019 |

17.0 |

13.0 |

17.0 |

21.0 |

16.0 |

11.0 |

7.0 |

5.0 |

|||

27.12.2019 |

17.0 |

19.0 |

13.0 |

15.0 |

17.0 |

19.0 |

21.0 |

16.0 |

11.0 |

7.0 |

5.0 |

* FX reserve requirement ratios for those banks fulfilling the real loan growth conditions stated in Communiqué No.2019/19 are applied as follows: 17% for deposits/ participation funds (excluding deposits/ participation funds at foreign banks) and Funds of Investments Banks with maturities shorter than 1 year and 13% for deposits/ participations funds (deposits/ participation funds at foreign banks) with maturities longer than 1 year.

After the revision, on 27 December 2019, the weighted average reserve requirement ratios for Turkish lira and foreign exchange liabilities stood at 3.6% and 16.0% (Chart 2.2.3.1 and 2.2.3.2).

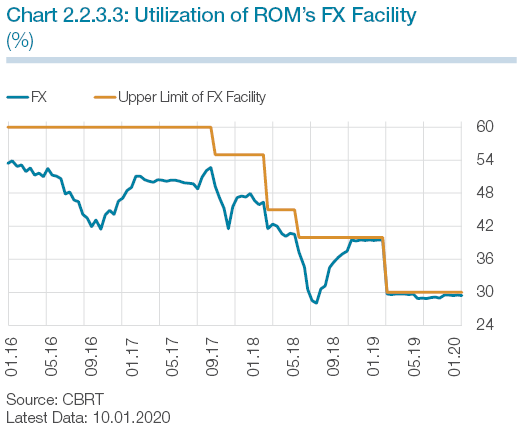

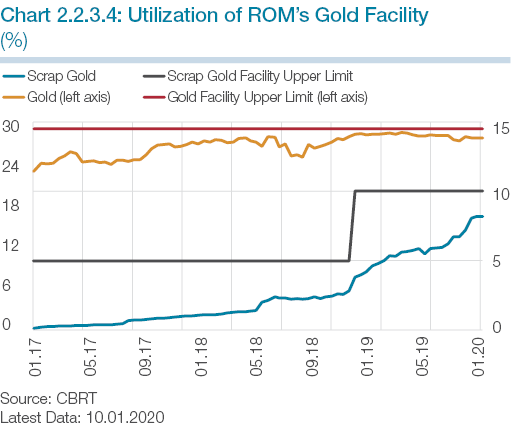

In the maintenance period pertaining to the calculation period starting on 27 December 2019, within the framework of the ROM facility, the rate of utilization was 98.2% for the FX facility, 95.5% for the gold facility, and 81.8% for the scrap gold facility (Charts 2.2.3.3 and 2.2.3.4). On the other hand, banks in Turkey can also maintain standard gold for their precious metal deposit accounts and this facility’s utilization rate was 81.3% as of the same maintenance period.

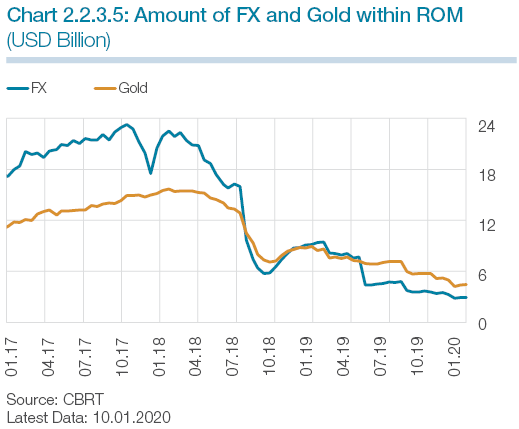

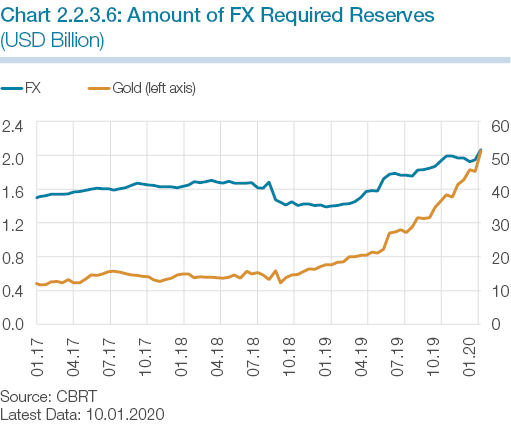

Again, the same maintenance period of 27 December 2019, USD 2.8 billion worth of FX and USD 4.9 billion worth of gold were maintained for Turkish lira liabilities within the framework of the ROM facility (Chart 2.2.3. 5). For FX liabilities, USD 51.7 billion worth of FX and USD 2.0 billion worth of gold were maintained within the framework of the ROM facility (Chart 2.2.3.6).

The aim of rediscount credits is to facilitate export companies’ access to credits with favorable costs and to reinforce the CBRT’s reserves. Rediscount credits, which are governed by Article 45 of the Central Bank Law, are extended in Turkish liras to exporters and firms that engage in foreign FX earning services and activities by accepting exporters’ FX denominated bills for rediscount through intermediary banks. The loans normally have up to 240-day maturities (360 days for exports of high-tech products and exports to new markets) and are repaid to the CBRT in foreign currency.

The total limit available for rediscount credits is USD 20 billion, USD 17 billion of which is assigned to Turk Eximbank and the remaining USD 3 billion to participation banks and other commercial banks and there has been no change in these limits in 2019. The credit limit, which is USD 400 million for foreign trade capital companies, is USD 350 million for other companies. The entire limit can be used in applications for credits with a maturity of up to 120 days, whereas a maximum of 60% of the limit can be used in credit applications with a maturity of 121 to 360 days. These limits are doubled for firms with a net sales revenue above TL 5 billion in last fiscal year, tripled for firms with a net sales revenue above 15 billion and quadrupled for firms with a net sales revenue above TL 20 billion.

Some arrangements introduced regarding rediscount credits are as follows:

In April:

In May:

In November:

Rediscount credit utilization, which was USD 22.9 billion in 2018, became USD 24.4 billion in 2019, with an outstanding credit balance of USD 17.3 billion by the end of the year.

Rediscount credits contributed to CBRT’s FX reserves by USD 22.7 billion in 2019.

The CBRT announces monthly maximum contractual and overdue interest rates to be applied on credit card transactions for quarterly periods. Table 2.2.5.1 shows these rates applied throughout 2019.

Table 2.2.5.1: Maximum Contractual and Overdue Interest Rates for credit Card transactions (%)

Periods |

Turkish lira |

FX |

||

|---|---|---|---|---|

Contractual Interest Rate |

Overdue Interest Rate |

Contractual Interest Rate |

Overdue Interest Rate |

|

Q1 2019 |

2.25 |

2.75 |

1.80 |

2.30 |

Q2 2019 |

2.15 |

2.65 |

1.72 |

2.22 |

Q3 2019 |

2.00 |

2.40 |

1.60 |

2.00 |

Q4 2019 |

1.60 |

2.00 |

1.28 |

1.68 |