MENU

MENU

MENU

MENU

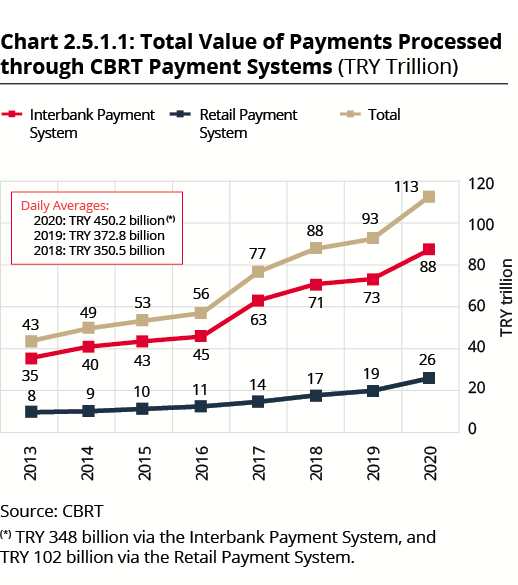

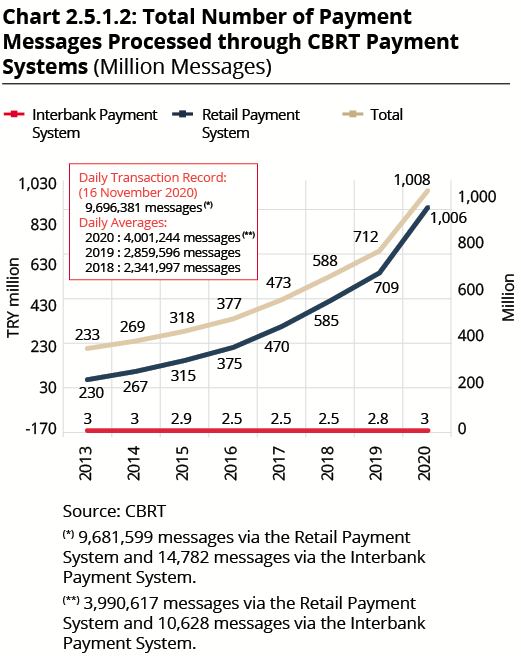

In 2020, the value of transactions conducted via the Interbank Turkish Lira Payment System and the related Electronic Securities Transfer and Settlement (ESTS) system totaled TRY 88 trillion, while the average daily transaction amount was TRY 348 billion. The number of transactions via the system was approximately 2.7 million in 2020, corresponding to 10.6 thousand payment messages processed per day on average. The amount of transactions settled via the Interbank Turkish Lira Payment System increased by approximately 19.4% compared to the previous year (Chart 2.5.1.1).

The total amount of transactions conducted via the CBRT Retail Payment System in 2020 was TRY 26 trillion while the average daily amount of transactions was TRY 102 billion. The number of transactions via the Retail Payment System in 2020 was one billion, corresponding to four million payment messages processed per day on average. The highest daily number of transactions as of end-2020 was registered at 9.7 million on 16 November 2020. The number of settlements carried out via the Retail Payment System in 2020 was approximately 41.8% higher than in 2019 (Chart 2.5.1.2).

The average daily number of messages processed in the auction system was 841.

With the inclusion of the Turkish Postal and Telegraph Corporation (PTT) in the CBRT’s Payment Systems on 23 October 2020, the number of participants reached 55 by the end of the year.

As part of its endeavors to modernize Turkey’s retail payment systems infrastructure to support innovative methods of executing and handling payments, the CBRT completed preparations for the introduction of a new retail payment system that will operate 24/7, enable end-to-end transfer of retail payments within seconds, and instantly notify the parties thereof. Named the Instant and Continuous Transfer of Funds (FAST), the new system will allow money transfers between accounts at different banks within seconds on a 24/7 basis.

The FAST System became operational on 18 December 2020 as a pilot run, and will gradually be put into full service. The final aim is to expand its use to cover all financial institutions in a short time.

Along with the FAST System, the Easy Addressing System, which enables users to initiate payments more easily by using data such as telephone numbers, ID numbers, or e-mail addresses, was also made available for use.

In the period ahead, the FAST System is expected to hold an important place in the payments ecosystem in Turkey and play a critical role in the development of innovative business models in the field of payments.

The Law No. 7247 Amending Certain Laws and Decrees entered into force following its publication in the Official Gazette No. 31167 on 26 June 2020. This law introduced amendments to the Banking Law No. 5411, the Law No. 5464 on Bank Cards and Credit Cards, the Law No. 6361 on Financial Leasing, Factoring and Financing Companies, the Capital Markets Law No. 6362, the Electronic Communications Law No. 5809, and the Law No. 6493 regarding Payment and Securities Settlement Systems, Payment Services and Electronic Money Institutions. Accordingly, it laid and reinforced the legal ground for the contractual relations regarding the financial services covered by these laws to be established through remote communication instruments besides the written form.

Before the Law No. 7247, there was no provision in Law No. 6493 as to the requirement of written form in the establishment of contractual relations between payment service providers and their users, and it was stipulated that the procedures and principles of the framework contract would be defined by the regulation to be issued by the CBRT. Establishment of contractual relations for payment services through remote communication instruments was already allowed in Law No. 6493 via secondary regulations. However, it was deemed beneficial to reinforce the legal ground of the related provision. Accordingly, a motion was proposed to the GNAT for the addition of a provision to Law No. 6493 to expand the form requirement for the establishment of contractual relations in many financial services and communication services.

Thus, paragraph three of Article 12 (on Payment Service) of Law No. 6493 stating that “The procedures and principles regarding payment services, the rights and obligations of the parties within the scope of payment services, information and conditions to be provided regarding payment services, and the framework contract are determined by the regulations to be issued by the Bank in consultation with the Financial Crimes Investigation Board (MASAK)” was expanded to include the following provision: “The framework contract shall be set in written form or by using remote communication instruments - distantly or not - via the methods which the Bank has determined to replace the written form, which will enable the verification of customer identity through an information technology or electronic communication device.” Work on the addition of detailed provisions to secondary regulations is in progress.

With Article 12 of Law No. 6493 on Payment and Securities Settlement Systems, Payment Services and Electronic Money Institutions in Turkey updated in November 2019, the main services of payment initiation and account information included in the Payment Services Directive-2 (PSD2), the European Union’s (EU) relevant regulation, were defined.

Work was carried out to determine the roles, liabilities and obligations of the parties, licensing provisions, and main operational and technical rules for these two new payment services via secondary regulations. Drafts prepared at the completion of this work on secondary regulations also included provisions regarding payment services data sharing services.

In line with these provisions, to determine the operational and technical requirements (API Standard and User Experience Documents) for payment services data sharing services, studies were carried out by a working group consisting of representatives from the CBRT and the Interbank Card Center (BKM). In this scope, global examples were examined, meetings were held with major central banks, and assessments were made regarding the establishment of an infrastructure aligned with Turkey’s needs that would ensure effective, efficient and safe operation. Accordingly, in view of the conditions and needs of our country, it was concluded that it would be useful to establish a technical service provider-focused application architecture for a fast integration of stakeholders and an efficient and effective experience of payment services data sharing services.

This architecture is based on an approach whereby the payment services data sharing services are offered by Account Services Providers through the BKM’s API Gateway in compliance with the to-be-developed national API standard. Following the related studies, the General Introduction Document for payment services data sharing services (PSDSS) was prepared, and the first drafts of the National PSDSS API Standard and user experience documents were drawn up in coordination with the stakeholders in the ecosystem (such as banks, payment institutions, and Financial Technologies (FinTech) already offering these services). These documents were disseminated to related parties to garner their feedback.

Enactment of the Statute of the Payment and Electronic Money Institutions Association of Turkey

The Statute of the Payment and Electronic Money Institutions Association of Turkey (the Association) was enforced following its publication in the Official Gazette No. 31169 dated 28 June 2020 upon the CBRT’s proposal and the Presidential Decree. Thus, pursuant to Additional Article 1 of Law No. 6493, the Association was established as a professional organization having the status of public legal entity.

With the Association Statute, the Association’s organs, duties and powers, working principles, scope of activities, and the terms of membership were determined. The members of the Association include payment and electronic money institutions (the institutions) operating in Turkey and licensed according to Law No. 6493.

The Association is composed of the General Assembly, the Executive Committee, the Audit Committee, and the Disciplinary Committee. It also has a General Secretariat. In the determination of voting power in the General Assembly of the Association, fifty thousand ballots are primarily distributed pro rata to the ratio of the institutions’ minimum equity capital liabilities to the sector’s equity capital liabilities. Then, the same amount of ballots is equally distributed to the institutions. The sum of ballots received via these two distributions constitutes the total voting power of each institution. The Executive Committee is composed of 13 full members (one of them being independent) and three substitutes while the Audit Committee and the Disciplinary Committee are composed of three full members and two substitutes each. Accordingly, nine full members will be elected to the Executive Committee to represent the institutions offering the payment services cited in the subparagraphs from (a) to (ğ) of Paragraph 1, Article 12 of Law No. 6493 (one member for each subparagraph); and three full members, three substitutes and one independent member having the plurality of the votes will be elected to the Executive Committee regardless of their field of activity.

The Association Statute vests the Association with the power to impose a disciplinary penalty on members of the Association upon the decision of the Disciplinary Committee and the approval of the Executive Committee. In addition, the Executive Committee has the authority to decide on the establishment of professional committees and other committees.

During the period before the organs of the Association were established, operations and procedures regarding the Association were carried out by the CBRT. In this scope, the CBRT received the membership applications of the actively operating payment and electronic money institutions in Turkey, and held the first General Assembly meeting of the Association. Hence, the organs of the Association were founded.

Enactment of the Regulation on the Generation and Use of TR QR Code in Payment Services

The Regulation on the Generation and Use of TR QR Code in Payment Services was introduced to establish the rules and principles for the generation and use of TR QR code in payment services. The regulation entered into force following its publication in the Official Gazette No. 31220 dated 21 August 2020.

The regulation makes the use of TR QR code compulsory in payment services covered by Law No. 6493, if and when QR code is used in these services. Additionally, it imposes various obligations on merchants and payment service providers regarding their TR QR code transactions. The regulation also includes a number of provisions concerning the preparation of Technical Principles and Rules Guidelines that will also cover workflows on a payment system basis or specific to a certain payment service, the issuance of a QR Code Generator Code required to generate a QR code, the establishment of the QR Code Routing System to ensure the transfer of QR codes and the information contained therein between payment service providers, and the determination of the display format to be used in workplaces to inform consumers that payment via TR QR code is available. Finally, the deadline was set as 31 December 2021 for payment service providers that currently enable payments via QR code to transition to TR QR code, and for merchants that accept payments through payment systems operated by the CBRT or through payment cards to build the infrastructure for TR QR code payments.

In addition, the “TR QR Code Technical Principles and Rules” document annexed to the Regulation defines the rules concerning the QR codes presented by both merchants and consumers as well as concerning person-to-person payments.

Due to the limited technical capacity of the existing POS devices, cash registers and ATMs, it is not possible for the majority of these devices to generate long QR codes that contain all the information required for payment in line with the TR QR Code Technical Principles and Rules. Therefore, to enable QR code payments with existing devices, the use of QR codes, called “short QR codes”, that contain less information than a normal QR code was also allowed.

To ensure interoperability between payment service providers in payments via QR code, including the short QR code, it was decided to build a QR Code Switching System at the BKM. The work on this system is about to be finalized.

In line with the regulation, work was carried out to prepare Technical Principles and Rules Guidelines, set the operating rules, participation terms and tariffs for the QR Code Switching System, and determine the display format used in workplaces to inform consumers that payment via TR QR code is available. The QR Code Switching System Rules document was published, and the Technical Principles and Rules Guidelines for TR QR Code documents were issued separately for card payments and for mobile payments via the FAST system.

Directive on FX Buying-Selling Transactions of Payment and Electronic Money Institutions’ Representatives

The Directive on FX Transactions of Payment and Electronic Money Institutions’ Representatives was delivered to institutions on 20 February 2020.

The directive was drawn up upon the letter of the Republic of Turkey Ministry of Treasury and Finance dated 5 February 2020 informing about the claims that representatives of Payment and Electronic Money Institutions were conducting FX buying-selling transactions besides money transfer transactions, and instructing that these representatives should be warned about the conduct of such transactions and that the written warnings, an example of which was attached to the Ministry’s letter, should be announced at the workplaces of the representatives.

The directive stipulates that institutions should warn the representative offices, excluding the authorized ones, about the conduct of FX buying-selling transactions as per the Law on the Protection of the Value of the Turkish Currency (Law No. 1567) and Articles 10 and 13 of the Regulation on Payment Services, Electronic Money Issuance, Payment Institutions and Electronic Money Institutions. In addition, it stipulates that written notices in Turkish and English should be put on the entrances, cash desks and the inside of the workplaces of these representative offices for customers to see that FX buying-selling transactions other than payment service and/or electronic money issuance transactions are prohibited and that both the workplace and the individuals will be subject to sanctions according to the Law No. 1567 if these transactions are conducted.

Directive on the Prevention of the Use of Offered Services in Illegal Activities

The Directive on the Prevention of the Use of Offered Services in Illegal Activities was delivered to institutions on 2 October 2020 following the analyses and evaluation studies on the problems in the sector and related solution methods that the CBRT conducted in close cooperation with other relevant public institutions and organizations, particularly with MASAK, upon the emergence of the issue of “intermediation in payments for illegal activities”.

In the scope of risk management activities conducted pursuant to Article 20 of the Regulation on Payment Services, Electronic Money Issuance, Payment Institutions and Electronic Money Institutions, the directive delivered to all payment and electronic money institutions calls for investigation of platforms including social media and online platforms to detect whether the services provided by institutions under Law No. 6493 are used in illegal activities, “illegal betting” in particular, and introduction of proper measures to prevent such transactions; appointment of special staff for this work, specification of the duties of these staff, and keeping a record of persons/accounts/cards/workplaces detected to engage in illegal betting and similar illegal activities as well as all related transactions; immediate reporting of these records to the CBRT and to relevant public authorities, MASAK in particular, depending on the nature of the illegal transaction; and keeping a record of online platforms checked and detected to facilitate illegal betting and similar illegal activities, and notification of them to the CBRT and MASAK.

Pursuant to the provision added as Paragraph 4 to Article 8 of the Law No. 6493 with the Law No. 7192 of 12 November 2019, the CBRT is authorized to be a shareholder of any systemically important system operator established and to be established to ensure uninterrupted operation of the payment and securities settlement systems.

The Interbank Card Center (BKM) operates pursuant to the license obtained from the CBRT and is considered as a system operator with systemic importance for the payment systems in Turkey due to the operations it conducts.

The CBRT has identified significant areas to improve in the payments infrastructure and innovative business methodologies in Turkey. Within the context of actions to be taken in this regard, in addition to its current roles with a focus on payments with cards, the BKM is planned to undertake significant tasks.

To this end, the CBRT has become the controlling shareholder of the BKM in accordance with Paragraph 4, Article 8 of Law No. 6493.

Operating License

One company’s application for operating license was approved and published in the Official Gazette.

Operating License for Other Activities

Seven applications for operating licenses for other activities that payment and securities settlement system operators may offer in addition to their principal activities were approved and published in the Official Gazette.

Transfer of Shares

Two payment systems’ applications for transfer of shares were approved.

Number of Payment and Securities Settlement Systems Operating in Turkey

As of 31 December 2020, there were eight payment systems and four securities settlement systems operating in Turkey pursuant to Law No. 6493.

Operating License

Four companies’ applications for operating licenses were approved and published in the Official Gazette.

Expansion of Activities

Two institutions’ applications for expansion of activities were approved and published in the Official Gazette.

Transfer of Shares

Five institutions’ applications for transfer of shares were approved.

Revocation of Operating License

The operating license of one institution was revoked, and the revocation was published in the Official Gazette.

Number of Payment and Electronic Money Institutions Operating in Turkey

As of 31 December 2020, there were 34 payment institutions and 21 electronic money institutions operating in Turkey pursuant to Law No. 6493.